Jan 2022

If you find this read interesting, share it on:

Wishing all our investors and readers a happy and prosperous 2022. After two difficult years, we hope that we steadily come back to normalcy in our daily lives.

The year has, however, started on a stressful note. India is now in the grip of a fresh wave of the Covid pandemic, most likely from the Omicron variant. It appears to be less lethal than previous versions, but we would still advise all our readers to be cautious and wear a mask, wash and sanitise hands and observe social distancing. We hope the present wave will not last long, but still request you to please avoid unnecessary risks during this period.

We remain constructive on Indian equities for 2022. The key driver would be the recovering economy, which, in turn, drives a strong and broad-based earnings recovery. There are two caveats though: the returns may not be as strong as the last two years and the sector leadership is likely to change in some ways. There will be some headwinds from the third Covid wave and rising rates, but there are enough positive drivers to overcome these.

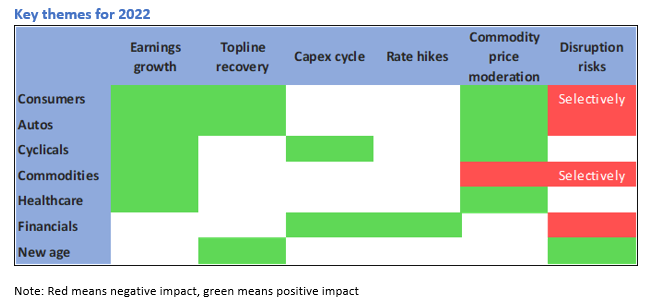

Our approach to 2022 is consistent with our recent strategy. We are focusing on consumers, cyclicals (ex-commodities) and exporters, underpinned by the key themes that we believe will define the next year. An additional filter is that we will be careful of high PE stocks unless there is strong earnings growth to support the valuations. We are selective on financials and are focusing on turnarounds and/or companies that are building capabilities to fight the fintech challenge.

SWEET SPOT FOR EARNINGS

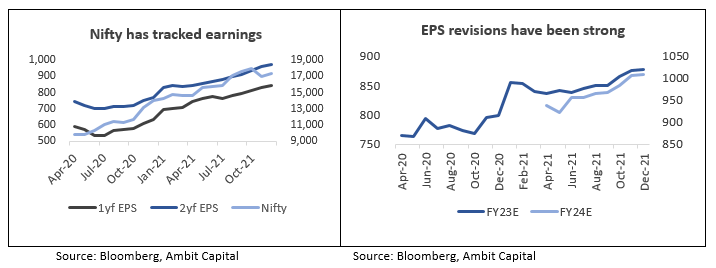

The narrative of the post-pandemic rally being liquidity-driven misses the underlying earnings momentum. The un-anticipated resilience of Indian corporates to the pandemic has turned the profitability story around. The Nifty’s 59.1 % jump (CAGR) from the 2020 low (23-Mar-2020) to end-2021 has largely tracked forward earnings (see chart below). It has been helped by continuous upgrades to FY23/FY24 earnings through this period.

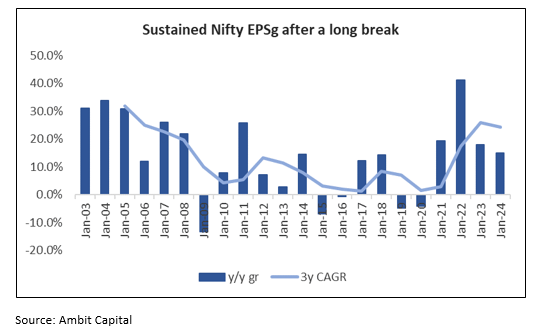

We think that this is just the beginning of the cycle. It is a combination of two factors: first, India is about to see a sustained period of 15%+ earnings growth over a 3 year period (FY21-24), something not seen since the noughties. Moreover, the earnings upgrade cycle is not done yet, in our view: the street is yet to fully capture the positive macro drivers in the economy.

The main risk to headline Nifty EPS growth would be composition changes – new age companies or large PSUs getting added. That, in our view, is largely mathematics and would not impact the market.

SUSTAINED GROWTH, AND MORE INCLUSIVE

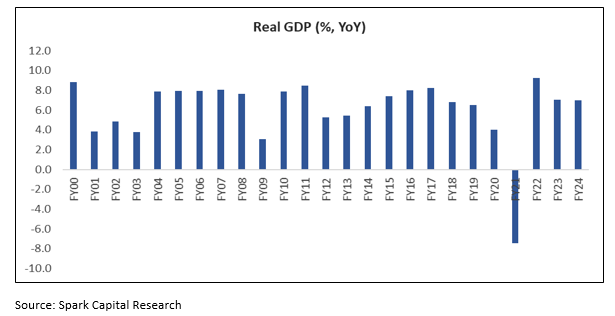

Growth should gather pace in 2022, enabled by a normalising economic activity with minimal lockdowns. There are other positive drivers in place: low real interest rates; improved revenues driving higher government spending and a strong global macro helping export sectors. We believe that India is starting a multi-year period of 7%+ growth, a trend not seen for more than a decade.

As the growth cycle lengthens, we expect the recovery to become more inclusive than in 2021. Lower-income groups could see a normalisation of incomes (and consumption). The enablers for these would be fewer lockdowns; a recovery in labour-intensive sectors like real estate and textiles; companies shedding cost-consciousness as growth returns and increased social spending by governments in the backdrop of local elections.

This is positive for the consumer stocks, which largely underperformed in 2021. Companies focused on a bottom-of-pyramid consumers should come out of the two-year funk as demand growth permeates through the layers.

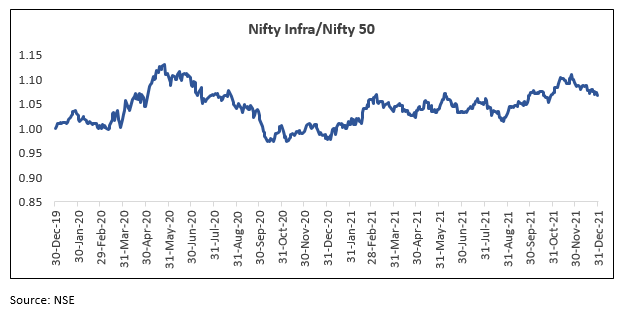

RETURN OF CAPEX, WITH A DIFFERENT FLAVOUR

India’s growth in the teens (2010-2020) was largely led by consumption, especially towards the latter half. The implosion of the steel and infra sectors killed India’s capex cycle, not least because the high NPAs choked credit to the sector. That period of funk has ended, and we see a new capex cycle emerging over the twenties. The nature of this growth will be different, largely by the government spending on infrastructure. The success of the asset recycling program is critical to this success. The private sector will not be left out, though: the real estate sector and, to some extent, manufacturing should also contribute to the recovery.

This may throw up long-term growth opportunities in India’s capital goods and construction ecosystem. Companies here also derive survivorship benefits – the ones that have lasted through the teens are, almost by definition, cost-efficient, well-managed with strong balance sheets. For investors, we expect lower risk and hence throws up opportunities. Some of this has already played out but we think there is still more upside in this sector.

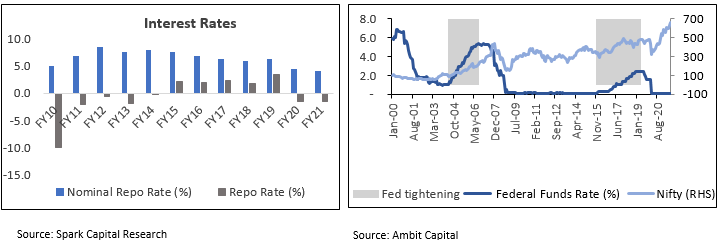

RATE HIKES NOT A PROBLEM

Rising rates (in India and the US) are unlikely to derail the growth. Parallels with the 2013 “taper tantrum” are misplaced as India’s macro stability indicators like the fiscal, current account deficit and forex reserves are now much more robust. There is unlikely to be a run on the rupee, and the RBI is in a much better position to defend it if there is. Domestically, India’s cost of capital is at a historic low, so a 50-100bp rise should not have an impact on aggregate demand. It will take 2-3 years of rate hikes to threaten growth.

We are not buying into the negative thesis on rate-sensitives. We feel that sectors like real estate and autos will be unaffected by rising rates at this early stage of the tightening cycle. Banks, in fact, could benefit from improved net interest margins (NIMs) as liquidity tightens a bit. These sectors may have other challenges, but not a demand weakness from rising rates.

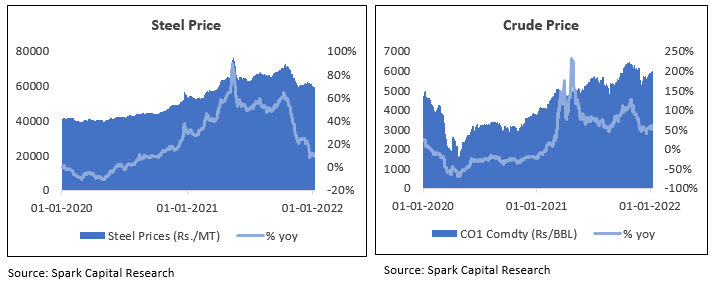

A BREATHER FOR COMMODITIES

The moderation in commodity price inflation should continue through the year. This is mainly due to the dissipating low base effect. Idiosyncratic factors like China supply shutdowns and rising US bond yields should also help keep prices in check. We do not expect a sharp correction in the base prices – just a slower rate of appreciation from here on (with greater volatility).

This may help consumer companies. The pressure on gross margins should start to ease – also helped by the post-Diwali price hikes taken across most segments. If commodity price inflation eases off, there will be no need to take price hikes and risks to demand growth in the coming year are mitigated.

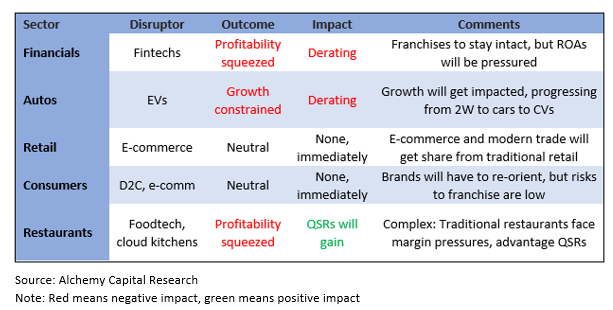

THE AGE OF DISRUPTION

We are at an inflexion point across many sectors that are being disrupted by new age technology. Incumbent businesses facing these challenges will not disappear overnight, but will face a combination of lower growth and margin pressures over the longer term. The challengers themselves may not be profitable, but they will nibble away at the incumbents’ lunch steadily. The process is getting accelerated by the huge pool of capital available to the start-ups.

This presents a double challenge to investors. Many legacy businesses are still standing on firm ground but are getting slowly derated. On the other hand, the start-ups are now entering the listed markets but are mostly unprofitable with poor financial metrics.

We are approaching this in a two-pronged manner. First, we are careful with adding legacy businesses that are getting disrupted. They are getting structurally derated, even if it the stress is not yet showing up in their operating or financial performance. They may deliver short-term performance in bursts but are not the consistent compounders they used to be. Second, we are selectively adding some of the listed start-ups to some portfolios. In doing so, our first step is to assess downside risk and we are avoiding the relative high-risk, high-return bets in this space.

Seshadri Sen

Head of Research

Alchemy Capital Management Pvt. Ltd

Source:

Alchemy Research

Bloomberg

7x5pjg85n7|00004A29|AlchemyStatic|ThoughtLeadership|Description

7x5pjg85n8|00004A29B796|AlchemyStatic|ThoughtLeadership|Description|D5A4BFAB-F423-4EF9-BB77-48618AFD9DB2