Sep 2019

If you find this read interesting, share it on:

Breaking the cycle of negativity

The surprise corporate tax cuts announced by the Finance Minister on Friday morning (20 Sep 2019) are a significant stimulus to the economy and markets. The benefit is not just a simple earnings boost to the markets, but also should have knock-on benefits to the consumption and investment cycles. Coupled with the aggressive monetary easing through CY19, this should break the cycle of negativity in the economy, even though it doesn’t solve all the problems in the economy.

Direct impact

The surprise factor should not be underestimated. There were no leaks of this proposed move in the media, and no policymaker had discussed this in recent times. The government had stated this as a long-term objective in 2014, but the recent policy debates had been focused on cutting GST for autos rather than using direct taxes to stimulate the economy. The unexpectedness of the move should contribute to turning sentiment around.

Earnings boost: The immediate tangible positive is, obviously, an earnings boost, particularly in the financials and consumer sectors. Most sell-side houses estimate the one-time earnings impact on the Nifty at 8-10%*. Over the longer term, this benefits balance sheets as ROEs move up and equity compounds faster (or dividends go up). Individually, the benefits to companies range from 5-15%, depending on the level of tax breaks being availed in the past.

Secondary positives

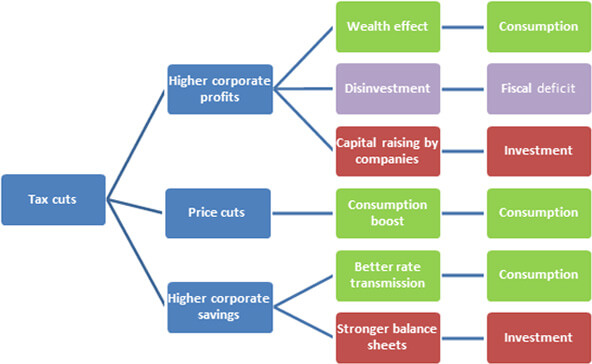

The benefits, however, go beyond the direct positives on earnings and stock prices. This is a fiscal stimulus, and its expansionary benefits on the economy could play out in a number of ways. Some of them may not be instantaneous, but the markets will discount these in advance, once visibility improves. The chart below illustrates the various scenarios that could unfold: it is too early to predict the direction in which this plays out.

*Impact on Nifty Earnings: Edelweiss Research –10% (FY20); Motilal Oswal – 8% (FY20, FY21); Spark Capital - 10% (FY20); FY20 numbers may be lower due to one-off DTL impact. Source: Sell-side reports, 21-22 Sep, 2019

Wealth effect: A resurgent stock market would help in boosting consumer sentiment through the wealth effect. Admittedly, the penetration of stock ownership in India is narrow and this would not be a broad-based positive, but businesses that cater to higher-income brackets could see an upturn.

Possible price cuts: Consumer and financial companies could pass the tax benefits to consumers via price cuts and lower margins, especially where they face demand challenges. This would be a logical step in sectors where pricing is reverse-engineered from target ROEs, like in banking. In other sectors, it would be tactical moves; probably led by players who are struggling for market share.

Investment cycle: The investment cycle is benefited from a number of angles. The new tax rates puts India at par with most competing countries, which would be a big positive for foreign investors – the 15%+ tax rate for new companies raises India’s competitiveness significantly. Investment decisions are a product of demand and expected returns: one leg of the equation receives a significant boost from this tax cut.

Monetary easing: We do not expect the RBI to pause on its path of monetary easing, and expect further cuts on top of the 110bp announced so far. Moreover, we expect monetary transmission to intensify in the coming months, now that we are into the fourth month of surplus liquidity. Sharp cuts in lending rates should help revive demand in certain segments, and we expect this to play out in early CY20, if not before.

Other positives: As we highlighted in our previous note, there are other positives in play, too. The positive monsoons and the wealth effect from higher gold prices augur well for rural demand. Some high-profile credit issues are getting resolved, with borrowers stepping up to sell assets where necessary (and possible). The real estate and credit markets still continue to be significant negative overhang, but there are some incremental positives there.

Key risks

Fiscal deficit: The tax cuts drive up the fiscal deficit by Rs 1.45 trillion or 0.6% of GDP. This can be mitigated by a) higher disinvestment and privatisation, with the buoyant stock market acting as an enabler and b) higher consumption would offset some of the revenue losses from the direct tax cut, though that may come with a lag. The fiscal stimulus does impede monetary transmission, but that could be overcome by the RBI continuing on its path of easing.

2QFY20 earnings: The stimulus has come too late to rescue 2Q earnings, which would be weak from the depressed demand scenario. Some of this is expected, but a strong rally into the earnings season could get destabilised by negative earnings surprises. A large one-time impact would come from writedowns in deferred tax assets – some of the larger banks are exposed to that risk in 2Q. The market may look through these as they are one-off, but the headline impact would be very large.

Our positioning

We are now accelerating our deployment in the markets, where we had been slower than our usual patterns in the recent past. We are not going “risk-on” and diluting our quality bias towards stock-picking, sticking to our overall GARP philosophy with an aversion to weak cash flows.

Seshadri Sen

Head of Research

Alchemy Capital Management Pvt. Ltd

7x5pjg85n7|00004A29|AlchemyStatic|ThoughtLeadership|Description

7x5pjg85n8|00004A29B796|AlchemyStatic|ThoughtLeadership|Description|47BBBBB6-E59A-4358-8F35-B87A30DF8887