Aug 2021

If you find this read interesting, share it on:

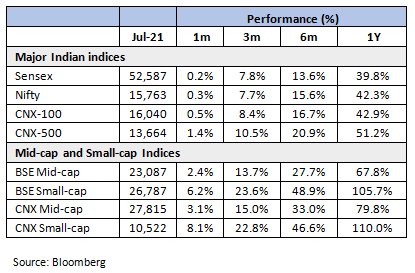

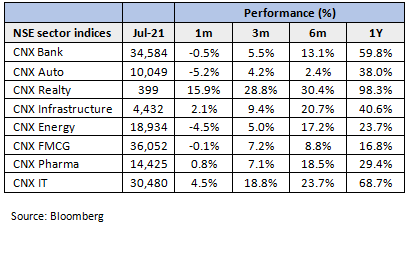

July’21 was another flat month for the indices (Nifty +0.3%) with interesting internals: small-caps and mid-caps outperformed with IT, consumers and healthcare the key sectoral leaders at the expense of financials and metals. The momentum, however, returned towards the end of the month. We remain constructive on the broader markets with tailwinds from the post-lockdown recovery, the strengthening investment cycle and earnings momentum driving it. Our focus remains on quality names with strong balance sheet, with a bias towards cyclicals.

Post-Covid recovery

We are seeing a gradual opening up of the economy as the second wave now seems to be receding. This has driven momentum in some sectors such as – banks, retail, and travel. We do see some opportunities in quality names in these sectors but remain selective and cautious for a few reasons.

-

The opening-up will be more gradual than the pre-Diwali phase last year, as governments will be more cautious given the ferocity of the second wave. An example is the reluctance of the Maharashtra government to open vulnerable venues such as cinemas and theatre. While some pent-up demand will undoubtedly play out, it may be more gradual than in CY20.

-

One uncertainty is how consumer sentiment plays out. The second wave had a much bigger impact on health and many middle- and upper-class families were affected by the tragedy. That may slow consumption propensity when the economy unlocks – we have to keep an eye on trends in each category.

-

Raw material inflation remains a challenge for most consumer-related sectors. The sharp rally in global commodities have forced most companies to absorb some of the margin impact and there appears to be no immediate respite. This headwind will be a factor for consumer company earnings for at least a couple of more quarters.

We see the short-term rally in some of these opening-up beneficiaries continuing for a while. We remain focused on the quality names in these segments, which can withstand the risks we highlighted above. Our pivot towards cyclicals, however, is not affected by these short-term trends.

Earnings trends

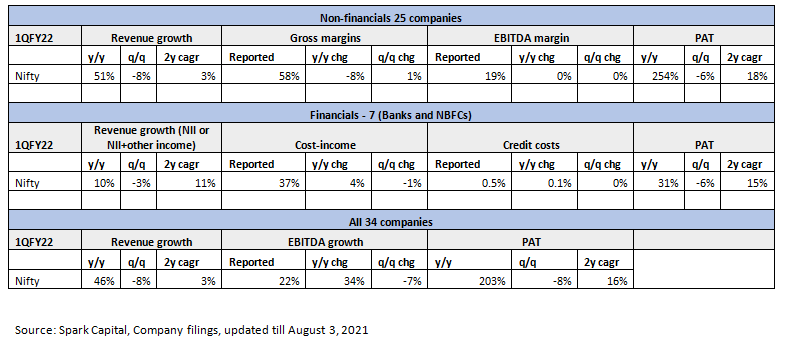

Earnings for 1QFY22 have been resilient through this quarter, despite the negative effects of the second wave of Covid-19. The y/y comparisons are coloured by a weak base, but the 2-year trends are positive with PAT growth at 16%, despite 3% top line growth. The margin performance is particularly heartening; in the context of the gross margin pressures (-800bps y/y) from rising commodity prices. The resilience of banks and NBFCs to the second wave has also been a significant positive.

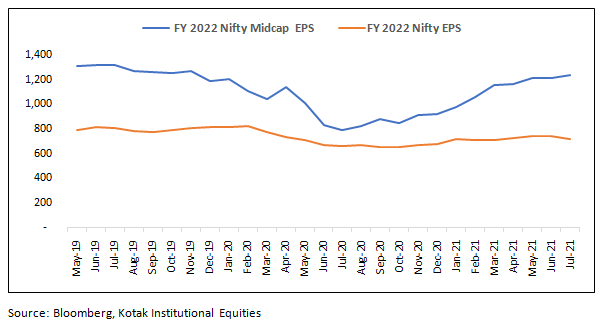

There has been, however, an impact on FY22 earnings estimates, and the upward revision momentum has reversed since May’21. This is mainly an adjustment for the 1Q sluggishness and the trend should now start to stabilise as the economy opens up. The pressure, however, has been asymmetrically felt by the large-caps, the mid-cap Nifty earnings remains resilient. This is driving some of the mid-cap outperformance of the last month.

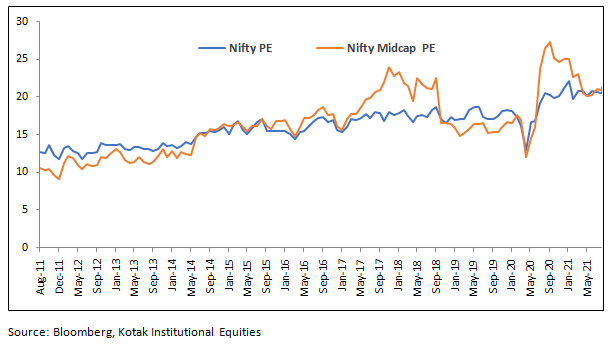

The momentum in midcap earnings is visible in how the relative valuations are playing out. After trading at a persistent discount through CY19, the midcap index PE is now at parity with the broader Nifty. In a recovering economy, we think that this works largely in favour of midcaps – the alarm bells go off when the premium significantly widens. Given the superior earnings momentum, it is likely that midcaps will outperform for the immediate future. However, midcaps generally carry higher risk, especially on liquidity when the cycle turns. We may increase our exposure to mid-caps, but in a measured manner with increased risk guardrails when picking the stocks.

Unchanged strategy

We are geared towards an upward-trending market. Our cash holdings remain minimal, and we aim to deploy as quickly as we can. We may increase our allocation towards cyclical sectors and mid-caps, while retaining significant guardrails on the quality of companies that we invest in.

Seshadri Sen

Head of Research

Alchemy Capital Management Pvt. Ltd

Source:

Alchemy Research

Bloomberg

7x5pjg85n7|00004A29|AlchemyStatic|ThoughtLeadership|Description

7x5pjg85n8|00004A29B796|AlchemyStatic|ThoughtLeadership|Description|7BDC18E1-9FEB-41AF-829D-B326DCBEF147