Feb 2026

If you find this read interesting, share it on:

The rapid pace of technological progress is reshaping the world around us. Today’s innovations have streamlined every stage of the development cycle—from idea generation to product launch—by improving efficiency, lowering costs, and enabling quicker feedback and iteration.

This wave of advancement has also had a profound impact on the investment landscape, making financial markets more open, data-driven, and efficient. Within this evolving environment, quantitative investing has risen to prominence, redefining how investment strategies are designed and executed.

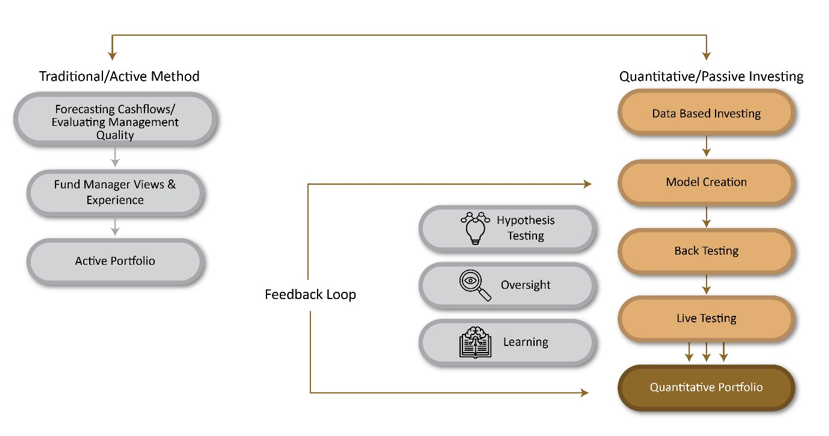

Unlike traditional funds, which rely on a manager’s judgment and experience, quantitative (quant) funds follow a fundamentally different approach to decision-making, risk management, and operations. Quantitative investing applies sophisticated mathematical models, statistical analysis, and computer-based algorithms to evaluate securities and market movements. By harnessing technology and vast datasets, quant funds create systematic, rule-based models, while conventional funds continue to depend primarily on human insight and intuition.

The structured process behind quantitative investing involves several critical stages:

-

Data Gathering and Evaluation: Quant strategies depend on large and diverse datasets, such as price movements, macroeconomic indicators, company earnings, news flows, and even market sentiment from social media.

-

Signal Development: Investment algorithms operate within the fund’s overall mandate—this may define the investment universe (largecap, midcap, smallcap, or multicap), asset classes, allocation strategy, time horizon, risk tolerance, and trading frequency, among other factors. Mathematical models then process the data to generate buy and sell signals in line with these predefined rules.

-

Portfolio Design: Using methods such as optimisation models, correlation analysis, and risk-adjusted return metrics, algorithms determine how capital should be allocated across securities.

-

Automated Trade Execution: Once the portfolio is constructed, trades are executed automatically through rule-driven systems, often breaking orders into smaller transactions to reduce market impact and improve efficiency.

Core Approaches in Quantitative Investing

-

Factor-Based Investing: Focuses on securities that display characteristics historically tied to superior returns—such as undervaluation (low P/E ratios), momentum (sustained price strength), financial quality (robust balance sheets), smaller market capitalisation, or reduced volatility. This method systematically combines these factors to build well-diversified portfolios.

-

Statistical Arbitrage: Aims to exploit short-lived mispricings between related securities through quantitative models. Common techniques include pairs trading and mean-reversion strategies, where positions are taken with the expectation that prices will move back toward long-term norms.

-

Risk Parity: Allocates capital by equalising risk contributions instead of following traditional market-cap weightings. The objective is to achieve balanced exposure across asset classes, thereby enhancing diversification and improving overall risk-adjusted performance.

-

AI and Machine Learning Models: Utilise sophisticated tools such as neural networks, random forests, and decision trees to uncover hidden patterns, forecast asset prices, and refine portfolio construction. These models can process vast and unconventional data sources—ranging from financial statements to news sentiment—to extract predictive signals.

-

Event-Driven Strategies: Build trades around market-moving events like earnings announcements, M&A activity, or key economic releases. Such models seek to capitalise on price swings and volatility that often follow these developments.

-

Smart Beta: Bridges passive and active management by creating portfolios that follow customized indices built on factor rules instead of simple market-capitalisation weighting. The goal is to achieve more favourable risk-return outcomes.

All of these strategies are built on strict backtesting, thorough data verification, and automated processes, which together ensure consistency, scalability, and discipline—distinct benefits that set quantitative investing apart from traditional, discretionary methods.

The shift from conventional investment styles to advanced quantitative techniques marks a major milestone in the evolution of modern finance. With rapid technological progress and the ever-growing availability of data, quantitative investing is poised to become an even more influential force in global capital markets, presenting investors and institutions with both vast opportunities and notable challenges.

Deven Ved

Co–Fund Manager, Quant

Alchemy Capital Management Pvt. Ltd.

Disclaimer:

-

Investments are subject to market risks, please read all product /strategy related documents carefully before investing.